Learn the differences between Debits and Credits in Bookkeeping, and make informed financial decisions. Discover the impact on small business accounting.

Bookkeeping is an essential process for any business that involves keeping track of financial transactions. In bookkeeping, every transaction is recorded in a ledger using a system of debits and credits. Understanding these concepts is vital to accurately and effectively track financial transactions.

In this article, we’ll provide a comprehensive overview of debits and credits in bookkeeping, including their definitions, how they work, and how to use them in everyday bookkeeping.

What are Debits and Credits?

Debits and credits are two sides of a transaction, and they are used to record all financial activities in the ledger. A debit is the left side of a transaction, and a credit is the right side of a transaction.

In bookkeeping, every transaction affects at least two accounts, and the total amount of debits must always be equal to the total amount of credits. This concept is known as the double-entry system.

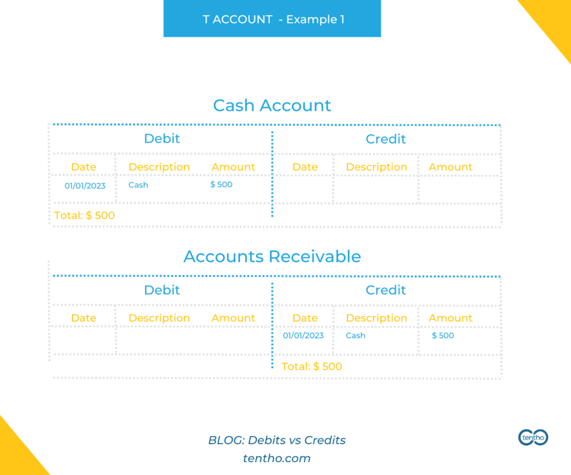

Debits and credits can be represented using T-accounts. A T-account is a visual representation of a ledger account, with debits on the left side and credits on the right side.

Debits and credits can be represented using T-accounts. A T-account is a visual representation of a ledger account, with debits on the left side and credits on the right side.

In the example above, the T-account shows a transaction where $500 was received from a client. The account “Cash” is debited, and the account “Accounts Receivable” is credited. The debit and credit amounts are equal, ensuring that the total debits and credits in the ledger balance.

Understanding debits vs credits in bookkeeping | Tentho | Example T Account

Understanding Debit vs Credit in Everyday Bookkeeping

To better understand debits and credits, let’s consider some common business transactions.

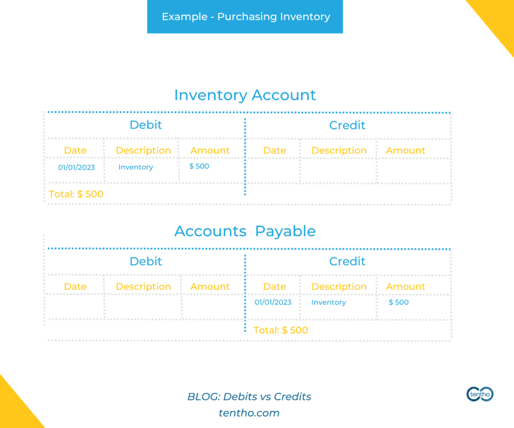

1. Purchasing inventory

When a business purchases inventory, the transaction is recorded as a debit to the inventory account and a credit to the accounts payable account.

Understanding debits vs credits in bookkeeping | Tentho | Purchasing Inventory

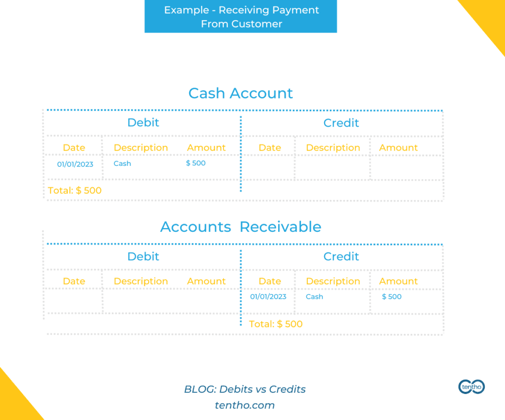

2. Receiving payment from a customer

When a business receives payment from a customer, the transaction is recorded as a debit to the cash account and a credit to the accounts receivable account.

Understanding debits vs credits in bookkeeping | Tentho | Receiving payment from customer

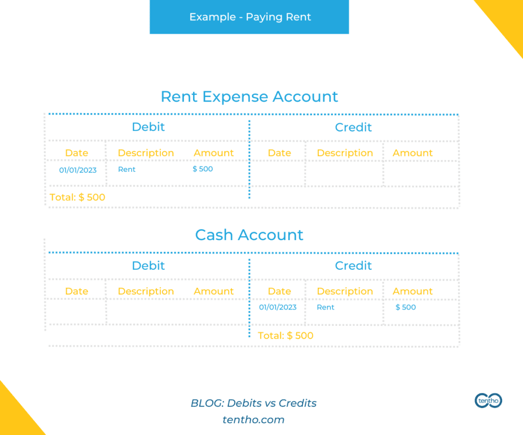

3. Paying rent

When a business pays rent, the transaction is recorded as a debit to the rent expense account and a credit to the cash account.

Understanding debits vs credits in bookkeeping | Tentho | Paying rent

These examples demonstrate how debits and credits are used to track financial transactions in everyday bookkeeping.

Rules of Debits and Credits

Debits and credits have specific rules that apply to different types of accounts. These rules are as follows:

Asset accounts

Asset accounts include cash, accounts receivable, and inventory. Debits increase asset accounts, while credits decrease asset accounts.

Liability accounts

Liability accounts include accounts payable and loans payable. Credits increase liability accounts, while debits decrease liability accounts.

Equity accounts

Equity accounts include owner’s equity and retained earnings. Credits increase equity accounts, while debits decrease equity accounts.

Revenue accounts

Revenue accounts include sales revenue and interest income. Credits increase revenue accounts, while debits decrease revenue accounts.

Expense accounts

Expense accounts include rent expense, salaries expense, and utilities expense. Debits increase expense accounts, while credits decrease expense accounts.

Conclusion

Debits and credits are essential concepts in bookkeeping that ensure all financial transactions are accurately recorded. By understanding the rules of debit vs credit, you can effectively track financial activities and create accurate financial reports. Using T-accounts is a helpful visual tool to help you understand and record transactions in a clear and organized manner.

In summary, debits and credits are the building blocks of bookkeeping. Understanding them is crucial for anyone responsible for recording financial transactions in a business. By following the rules of debits and credits, you can ensure accurate financial records and make informed business decisions.

Unlock your potential and navigate the complexities of your industry with Tentho as your guide! We're passionate about providing insights and inspiration to fuel your journey. While this post is crafted to enlighten and empower, it's important to complement this knowledge with tailored advice. We encourage you to consult with your own legal, business, or tax professional to address your unique needs and circumstances.

At Tentho, we're committed to your success and stand ready to assist you in understanding the broader landscape. However, please note that Tentho does not accept liability for any actions taken based on this post. Your informed decisions, guided by personal consultation with experts, are crucial to your achievements. Let's collaborate to make informed decisions that propel you forward, ensuring that your triumphs are as personal and impactful as your aspirations

Is your business inventory heavy? Discover what the 3-Way Match in Accounting is, how it can help, and the pros and cons of this approach.

Giuseppe Garcia-Salamone

Aug 23, 2023

GET OUR NEWSLETTER

Stay in the Know: Subscribe to Our Monthly Newsletter

Join our exclusive monthly newsletter to receive expert insights, industry trends, valuable tips, and special offers straight to your inbox. Don't miss out on the latest resources and strategies designed to help your small business thrive.